As with most English monastic communities by the early thirteenth century, parentage, institutional structure, and monastic activity can all be traced to the father of Western monasticism. The requirements of prayer, meditation, discipline, duty, and work which were imparted through the practical and theological wisdom of St. Benedict (480-543) within his Rule was why the function of these foundations became more than simply a hub of faith. Instead, through his Rule, monastic sites became bustling homes of learning which nurtured the study of theology and arts whilst also incorporating agriculture, economic administration, and land ownership. This structure achieved such popularity that both the priory and abbey at Canterbury belonged to the Order of the Black Monks of St. Benedict.

The creation of a reformed Order, as well as a new pastoral and administrative structure by Archbishop Lanfranc, was instrumental in providing this large and diverse constituency with intellectual power, leadership, and economic precision. The system of the obedientiaries (high officials) which arose from this reorganisation will thus be the focus of this article as they provide a particular insight into the topography of Christ Church and its great officers whom monastic activity revolved around. Understanding the obedientiaries of Canterbury alongside the prior will provide insight into the importance and complexity of these offices.

Domestic Affairs

Before delving into the domestic offices, however, the prior should first be examined as he was the pinnacle of the community and its affairs. Although the archbishop was, in effect, the true summit of the monastic hierarchy within the cathedral priory, he was rarely present after the first half of the twelfth century. As such, the prior stood in loco abbatis and exercised power and influence almost equal to the archbishop. In fact, from a social standpoint, the prior was almost indistinguishable from a contemporary great feudal magnate. Whilst during the Saxon period the prior, known as decanus et munuc, was elected by the archbishop, by our period in question the structures of the election had significantly changed. In 1174, Pope Alexander III granted Christ Church the privilege to elect their own prior, so long as he was a member of the Canterbury community and could fulfil the role suitably. This was confirmed by Urban III in 1187 who also added that the prior should not be deposed, save for the gravest reasons. Pope Gregory IX (1227 – 1241) also specified, most probably due to the events of the exile of the monks in the early 1200s and jostling between the king and papacy, that the election of the prior belonged solely to the monks.

This was a highly contentious matter which resulted in frequent clashes between the Christ Church monks and the various secular and ecclesiastical authorities over their power to elect. To navigate such tensions, a system seems to have emerged in the early thirteenth century whereby the monks submitted potential candidates to the archbishop for final review. As such, although the monks had the right to appoint their prior, the archbishop reserved the right to make the final decisive decision. This was not, however, entirely successful and the prolonged periods of vacancy between priors represent occasions where there were disagreements over succession. Ultimately, the tensions and privileges which underpin the succession of the Canterbury prior demonstrate the extent to which it was a keystone pillar of the monastic community.

Although the prior was urged to live amongst the monastic community in accordance with the Rule, his role made it inevitable that he would be absent for prolonged periods. As such, a series of sub-priors, or priores claustrales, were appointed to represent his will and command. The main role of the sub-prior was to undertake periodical inspections of the other obedientiary offices and report on any forms of mismanagement or breach of discipline.

The following examines the group of obedientiaries who dealt with the domestic, and somewhat secular, affairs of the priory. The first of which, the cellarer (often accompanied by a sub-cellarer), held a key position in the administration of the household and its bodily life.

The cellarer, in its purest form, was in command of the food and drink supplies at the priory, but he also ordered building materials for damaged buildings and fuel. Not only did servants, monks, and other dependents rely on him, but so did millers, bakers, cooks, and brewers for their raw resources. As such, the cellarer was often absent from the priory, acquiring produce from granges, markets, farms, and fairs. He was so integral to the household that he was granted a special privilege of absence from religious ceremonies, offices, and prayers on the promise that he would undertake these privately on his travels. Not only was he provided with special permissions, but the cellarer was also afforded the largest revenues amongst all other obedientiaries.

When understanding the cellarer expenses across the whole period from 1213 to 1230, some notable results arise. In the year that the monks return from exile at the hands of King John, the expenses are incredibly low, only £301 13s. 7d. In the following year, as the income streams began to return and money was injected into the priory, the total expenses of the cellarers rose and stabilised at around £850-£900. The cellarer’s expenses, as well as the total income and expenses of the priory, suddenly diminished from 1215 to 1217. This period coincided with the First Barons’ War, and more specifically the siege of Dover and control of the region by Louis, son of Philip Augustus of France which heavily impacted Kent and the surrounding counties. The total expenses of the cellarers at that time were between £200-300. As the war finished and financial recovery occurred, the expenses of the cellarer also increased. Then, in 1220, at the year of the Translation of Thomas Becket, the cellarer's expenses dramatically rose to £1154 16s. 5 ob, namely because of the grand amount of wood and wine purchased for the ceremony. What is then particularly interesting is that the expenses of the cellarer then slowly decreased each year following the Translation. This was most probably due to a relaxation in pilgrims and thus a decrease in the income which could be redistributed internally.

The cellarers had an especially high expenditure above other departments, and the reason for this was due to the vast number of monks and potential guests that they had to provide for twice a day. Whilst two standard meals, one (prandium) at midday and the other (cena) at around 5pm, may not seem a great deal, Gerald of Wales comments on the luxurious banquets served at Christ Church at the end of the twelfth century. On one Trinity Sunday, he recounted with great delight that no less than 16 courses were served firstly to the prior, and then to privileged individuals and monks. Records corroborate this splendour by demonstrating that bread, fish, eggs, and poultry were all commonly consumed within a meal at the refectory. Alongside standard meals, the cellarer also had to prepare for the many monastic occasions for celebration and feasting. Detailed in the anniversarian’s accounts are records of food allowances made to monks on obit-days of priors and archbishops. On High Mass, extra rations of food were also given to monks for celebration. As such, the monastic community at Christ Church had an impressively high standard of living which was maintained by the cellarer and required precise planning. There was, however, a controversial exception to the culinary menu of Canterbury Priory as St. Benedict forebode the practice of eating meat within his Rule. This practice was upheld from as early as 960 until 1216. Whilst after this period meat could be eaten in selected places, in 1225 the accounts show that the cellarer bought no meat at all. Instead, varieties of fish and poultry were depended upon alongside cheese, eggs, and vast amounts of bread.

There were three main loaves consumed at Christ Church. Panis monachalis, also known as panis conventus, was a wheat-based bread served at the monk’s table along with small loaves known as smalpeys, and playnpayn. A barley-based loaf of lower quality, feytis, was also commonly eaten amongst servants of some importance. Those at the bottom of the hierarchy were given a coarse, mixed-corn loaf to be satisfied with. Alongside the vast amounts of bread consumed were copious amounts of wine. Gerald of Wales remarks also that many wines, both mulled and clear, together with mulberry wine, unfermented, and mead were served in the refectory of Christ Church. The treasurer accounts of 1220 show that the purchasing of wine accounted for £190 15d. ob, or around 16% of the total cellarer expenses. Such a vast amount was to meet the demands of the bustling crowds attending the Translation, but the expenditure on wine in other years was not overly too far off as in the following year, £84 9d. was spent as part of the cellarer’s expenses.

Aside from food and drink supplies, there are several other expenses listed within the accounts which were attributed to the cellarer. Wood, alongside wine, was also a large expense of the cellarer’s accounts which may well have been used for either fuel or building materials. Typically, these expenses ranged from as little as £53 to as much as £215. In 1221, however, the sum of expenses for wood was an astonishing £431 17s., almost half of the total cellarer expenses for that year. Furthermore, considering the extent to which the cellarer travelled throughout the year, it was no surprise to see that a horse and cart were listed amongst the cellarer’s expenses for £10 in 1219 and £7 in 1220. Equally, in 1218, £14 13s. was also attributed to the cellarer for hay for his travels.

It should be noted, however, that all these expenses were divided up amongst multiple cellarers within a fiscal year. Historians have written very little about the number of cellarers at any given time, nor the turnover rate of the position. Despite this, the treasury accounts of 1222 from manuscript DCc/MA1 provide a glimpse into the structure of the role by stating the following:

Cellarer John Crundale: Expenses from the feast of St. Michael to the feast of St. Martin

Cellarer Richard: Expenses from the feast of St. Martin to the feast of St. Thomas the Apostle

Cellarer John of Roffa: Expenses from the feast of St. Thomas to the feast of St. Michael

This demonstrates that multiple cellarers worked on a rotation and divided the year into three periods. What was peculiar, however, was that there was not a fixed date of rotation, as corroborated by the accounts of the following year which state:

Cellarer John of Checham: Expenses from the feast of St. Michael until the vigil of St. Jacob

Cellarer John of Crundale: Expenses from the vigil of St. Jacob until the feast of St. Michael

This would give the impression that the rotation of office was divided irregularly amongst the number of cellarers of that year, with some cellarers in office for as little as 2 months, or as many as 9 months. Whilst the reasoning behind the choice of these dates and rotation periods is uncertain, it does demonstrate that the structure of the role differed vastly from the prior. Rather than a permanent position, the offices of the obedientiaries were temporary. The prominent reason behind this was that an individual cellarer was feared to wield too much influence and wealth, and thus a high-turnover rate made it impossible for any single cellarer to become a threat to financial unity.

Although true, this did not mean that a certain cellarer could not return to his position. Taking a step back to understand the manuscript in a wider scope, we see that John of Crundale was listed as a cellarer in 1222, 1223, 1224, and 1225. Equally, a cellarer named Radulf was listed as holding his position in office from 1225 to 1227 and in 1229 (presumably also 1228). Lastly, another cellarer named William held his office from 1214 until 1217, and a cellarer named Richard held office from 1218 to 1221. Thus, whilst a rotation of office within the fiscal year does occur, the respective cellarers held their position for prolonged periods of around three years.

The cellarer, however, worked closely with a lesser obedientiary, the garnerer. Situated on the north-side of the curia, the predominant role of the garnerer was to oversee the granary for wheat. Next to the granary was the bakery where the loaves listed previously would be baked for the respective meals by servants under the watchful eye of the garnerer. Flour was typically purchased by the cellarer or garnerer from the various mills owned by the priory. The expenses of an individual garnerer varied quite drastically; in 1217, as little as £4 15s. 6d. was spent, whilst in 1220, over £290 was credited to them. It is noteworthy that the proportion of this expense which was earmarked for purchasing wheat was very small. In 1216, of the £34 4s. spent by garnerer Luke, 58s. 8d. Ob was used to purchase wheat from Pecham. The rest, most probably, was used to maintain the granary and pay the servants. Unlike the cellarer, the structure of the garnerer role was as flexible as their expenses. Whilst in 1213, only one garnerer was listed as William, by 1215, as many as four garnerers; Luke, Alexander, Herlewin, and Andrew are provided, and in 1216, another garnerer, Richard, was added. Then, in 1217, only two are listed, Hubert and Richard. The reasoning behind such a chaotic structure was uncertain, but perhaps the granary was afforded more flexibility and freedom with its employment as it was a very small threat to the grand scheme of financial unity and aided in limiting the influence of the cellarer.

Alongside the cellarer, another prominent obedientiary who was key to the daily life of the community was the chamberlain, or camerarius. Unlike the aforementioned obedientiaries, this office was shown in the accounts to only contain one official with an assistant. There was an instance in 1213, however, of two chamberlains being listed within the accounts. This was potentially a temporary measure to ensure a quick recovery after the exile, or an overlap of obedientiaries when the returning monks had re-joined those who remained. Be as it may, it is clear that the expenses of the chamberlain follow a similar pattern to the cellarers but at a much lower amount. Whilst the chamberlain also witnesses a decrease in expenditure as a result of the First Baron’s War, the Translation does not appear to make overly much difference to how much was spent. This was most probably because the role of the chamberlain focused predominantly on the monks, and thus he did not have to accommodate the vast numbers of pilgrims in the same way that the cellarer did.

Although the expenditure of the chamberlain was much lower than the cellarer, the chamberlain, along with a sub-chamberlain, was equally as integral to the priory. They oversaw the clothing, accommodation, laundry work, washing, and shaving of the monks and servants. The chamberlain was primarily based within the tailor’s workshop within the precinct and purchased a variety of goods to make into garments. According to the Rule, precise rules and regulations governed the size, shape, and design of the black habit, and as such, black cloth was typically the leading expense in the chamberlain’s account. Maintaining a large cohort of monks with garments, soaps, and other amenities would have been a grand undertaking. As such, it was common for the chamberlain, like the cellarer, to also venture to fairs and markets to purchase cloth, linen, pelts, and leather, as well as sewing materials and bathroom necessities. Whilst he was not strictly afforded the same special privileges as the cellarer, the chamberlain was sometimes excused from prayers and ceremonies to fulfil his role if needed. What was particularly notable, however, was that a proportion of money, only 50s., was attributed within the accounts of 1213 and 1224 to the chamberlain for a “domum in Hoilande”. R.A.L Smith writes that from the fourteenth century, monks purchased “the best Flemish cloths for their garments”, and in 1318, the Canterbury foreign agent purchased over 200 Frisian cloths. It was, therefore, possible to propose that this particular expense could have been an early formation and establishment of the economic cloth trade between Canterbury and the Low Countries in the following century.

Aside from cloth, a common expense of the chamberlain was soap, which was to be used for compulsory baths at Christmas and optional baths throughout the rest of the year. For smaller occasions, the chamberlain was tasked with providing hot water, towels, and soap among other cleaning amenities. And whilst there was no definitive site of a laundry-room at Canterbury, lists of washer-women illustrate that there was a structure in place for habits, shirts, drawers, and socks to be cleaned every fortnight in summer, and every three weeks during winter. This, as well as upholding a system of tallies to ensure items were returned to the right monk, was maintained solely by the chamberlain and his assistant.

The remaining obedientiaries tasked with the domestic affairs of the priory were the refectorarian, infirmarian, and master of novices. Whilst these officers are not mentioned within the treasury accounts, it was worth discussing them briefly to understand their role and contribution to the wider cathedral community. The first of which, the refectorarian, worked closely with the cellarer to supply the refectory with utensils and necessary tools. The infirmarian was primarily in charge of the infirmary, which was not just an accommodation for the sick, but also those who were too infirm for daily duties as well as monks who were bloodletting. The infirmarian, however, oversaw the whole wing to the east of the cloister and therefore the hall, chapel, dining-hall, and kitchen were within their control. Nevertheless, within the infirmary was a resident physician and bleeder who relied on local oculists and apothecaries for herbs, cordials, lozenges, and ointments for the sick. The prior, however, reserved the right to see a specialist or consultant in London for a hefty price. Finally, the master of novices was instrumental in teaching the Rule and divine office to novices and monks. He may well have worked closely with the precentor or succentor, who will be discussed in the following section, as a subordinate for educational work. His role, as with the refectorarian and infirmarian, required few expenses and thus his appearance within records at Christ Church is uncommon. Nevertheless, he taught the young monks about monastic life, daily routine, and discipline without succumbing to impulse. Even recreation was a key part of a monk’s life, and the master of novices was key in promoting both indoor and outdoor activities which all participated in.

Spiritual Affairs

The primary role of the precentor was music. And whilst some of his duties were delegated to the succentor (such as teaching the young monks how to sing, recite psalms, and chant prayers in precession), he was responsible for the usage, supply, and condition of books as well as the materials used to copy books such as parchments or skins. His duties as a librarian also made him an instructor, holding daily classes in the cloister for novice monks and Latin classes in a room on the western side of the southern cloister-walk. As such, the precentor rarely features in the financial accounts and so sources on his day to day life are somewhat slim.

The soul of the priory, however, was the church, and according to St Benedict, “nothing was to be preferred than the opus Dei.” Whilst the precentor and succentor are prominent figures within this divine service, the sacrists and their assistants were integral to the fabric of the church and the maintenance of the allegory of God upheld within the spiritual precinct. The sacrists, credited within the financial accounts as being two in number but known to have up to four assistants alongside them, oversaw the repair, extension, and improvement of the church as well as its shrines and altars. Equally, they oversaw the task of lighting and cleansing the church as well as maintaining its curtains, ornaments, sacramental vessels, and vestments. If the cellarer was crucial to the bodily life of the priory, then the sacrist was integral to its spiritual being. The sacrists and sub-sacrists would light the cressets and bowls of tallow to illuminate the cloister, nave, choir, and treasury after dark, and would awake before the brethren at midnight to light the dormitory before matins. The sub-sacrists also stood as guardians of the shrines and altars, and it was not uncommon for them to sleep in the last chamber and choir to safeguard the treasures and relics.

As such, the expenses of the sacrist were relatively high. As discussed in the previous article, the expenses of the sacrist were also impacted by the Baron’s War and Translation. What was particularly interesting about the expenses of the sacrist, however, was that the Translation of Thomas Becket itself was not the year with the highest expenditure. Rather, expenditure increases in the following four years, perhaps due to the rising income from the shrines and altars. Nevertheless, the period from 1225 to 1227 witnessed a drastic downfall until 1228 when the expenses begin to rise again. Whilst a relaxation of expenses after the Translation is witnessed within other departmental accounts, the sudden rise in 1228 may have been prompted by the calling of the Sixth Crusade. The accounts from this year onwards include payments to a dominus Ricardus crucesignatus, and so it was not entirely farfetched to conclude this increase as being related to the crusade.

Within each year, however, these expenses were typically the result of purchasing lead, glass, and other raw materials from workman fairs, as well as wax, tallow, hay, and straw from farms, and on occasion charcoal, wine, and incense. Wax alone had cost between 5d. and 7d. per pound when bought in bulk, and the accounts of 1223 show that 300lbs of wax was purchased at £6 15s. by the sacrist through the feretrarians. Wax was a hefty expense for the sacrist, especially when consideration is made for the fact that they had to maintain the candles of the whole monastery. The East Candle, known as cereus paschalis, contained 300lbs of wax alone. Combine this with the 50lbs of wax needed for the seven-branched candelabrum, the 3lbs of candles require on the feast of Purification, and the 2lbs of candles carried in processions, it was not surprising that a large amount was spent on just wax.

As mentioned, the treasurer accounts note two sacrists for most years: Andrew and Roger are credited in the financial accounts as the sacrists from as far back as 1207 until 1219, Herlewin was then solely mentioned alongside a sub-sacrist Hubert from 1220 until 1226, whereby from 1227 until 1230 (and presumably further), two sacrists are named as Bartholomew and John. Given that they were as integral to the spiritual life of the priory as the cellarer was to the bodily life, they may well have rotated on fixed periods. This is uncertain but demonstrates that these roles required a team of monks to be sufficiently undertaken.

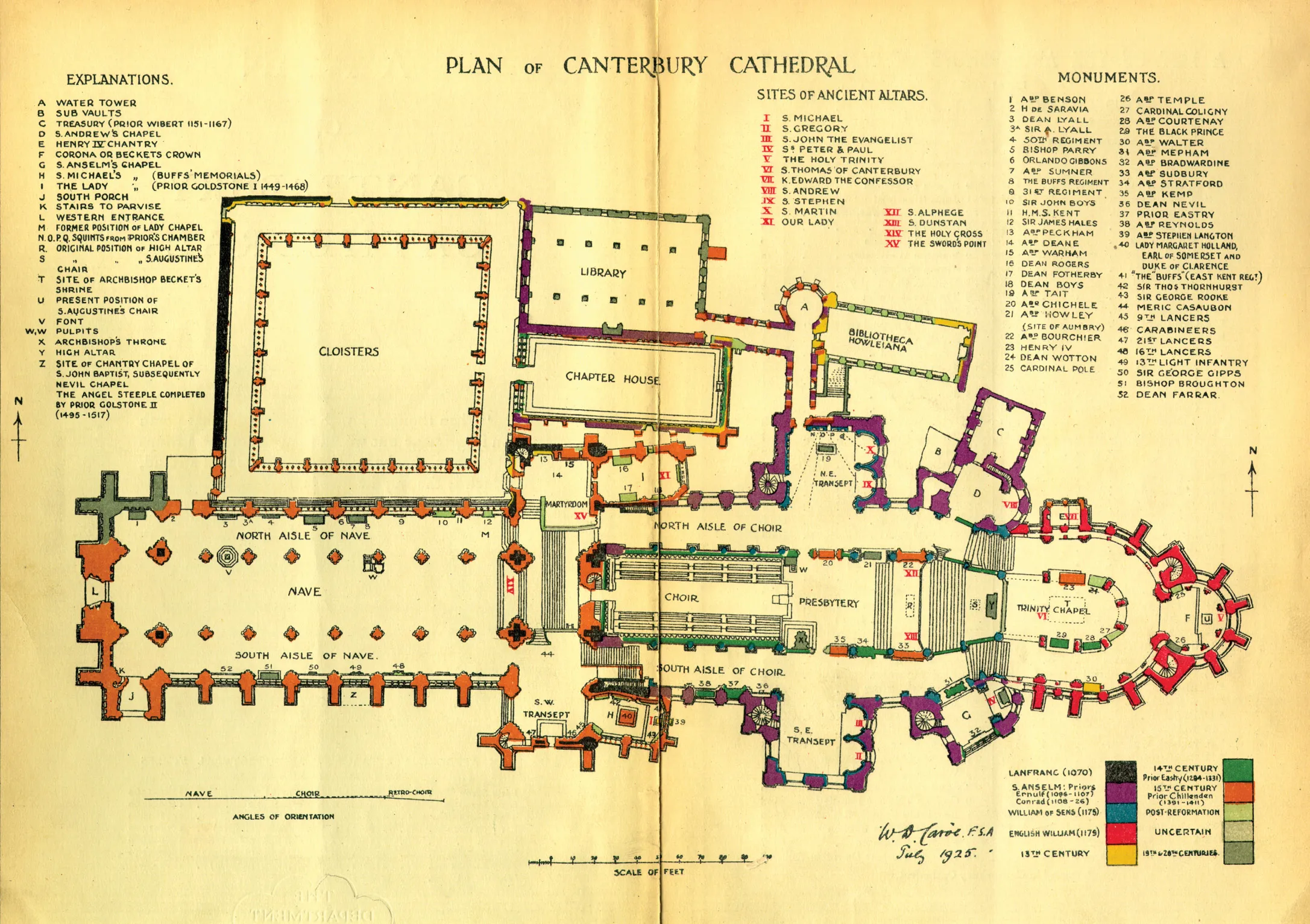

Most important of all in regard to the spiritual essence of the monastic body were the shrine keepers. From 1198, the Treasurers received all offerings made at the following altars:

The Tomb of St. Thomas, situated in the crypt.

The Altar of the Martyrdom, positioned in the north-western transept.

The Corona, located at the eastern extremity of the church.

The Shrine of St. Thomas (After 1220).

The High Altar.

The Altar of St. Mary, located in the nave.

The Altar of the Cross, also in the nave.

The Altar of St. Michael, situated in the south-western transept.

During the pre-exile years, the offerings attributed to these shrines and altars averaged around £426 3s. 7d. per year, of which the Tomb gathered £309 5s. 0d., Corona £39 17s. 6d., High Altar £39 19s. 10d., St. Mary’s Altar £8 9s. 0d., Holy Cross £1 2s. 0d., and St. Michael’s Altar 16s. 3. During this period, the total revenue of Canterbury was £1,406 1s. 8d. meaning that the offerings contributed over 30% of the total income. The offerings were highest in 1200-1201 when King John and Queen Isabella were crowned by Archbishop Hubert at Canterbury. During this period the offerings amounted to £620 4s. 0d. Compared to pre-exile figures, the offerings never fully return to the £426 average. Rather, the average from 1213 – 1230 sits between £350-£400. Nevertheless, there is a considerable increase in 1220 which is marked by the Translation of St. Thomas Becket as well as the 50th anniversary of the archbishop’s murder. The treasury accounts lack a definitive reference to the construction of the shrine but given that the rather unhelpful reference ‘ad diversa negocia’ (various investments) also increases this year to £465 2s. 8d. it is probable that the shrine’s construction fees were incorporated here alongside the payments for the bull of indulgences from Pope Honorious III.

Nevertheless, this event is recorded by contemporaries as quickly becoming a major festival. During the whole celebration, which lasted two weeks, hay and provender were provided along the entire pilgrim route from Canterbury to London. It is also reported that a banquet was held four days prior to the ceremony which reportedly catered for 30,00 people. This is reflected within the accounts as £1154 16s. 5 ob. of the £2307 18s. 2d. of total expenses in 1220 was earmarked to the cellarers for these abnormally high provisions required for the overwhelming number of pilgrims. Considering that, in the previous year, the amount allocated to the cellarer was £442 8s., this would demonstrate a 161% increase in allocated expenditure for the office. On the actual day of Becket’s translation, wine is reported to have run in the gutters. The treasurer’s accounts of this year show that £190 15d. Ob was spent on wine alone which is over double the amount spent in the following year. The amount spent by Langton on the ceremony was so large that they were still being paid by Archbishop Boniface in the 1240s. A large proportion of this expenditure was allocated to, as Matthew Paris states, providing a coffer covered with gold and jewels for the saint to rest in more honourably. The newly built shrine, however, was not the only shrine to receive vast numbers of pilgrims. The receipts of the individual altars were as follows: High Altar £54 15s. 8d., St. Mary £13 4s. 9d., St. Cross £2 9s. 8d., St. Michael 14s. 5d., Shrine £702 11s.4d., and the Martyrdom £93 0s. 2d.

Whilst 1220 – 1223 suggests a relatively successful period of attracting pilgrims, all of the shrines and altars witness a steady decrease in revenues after the Translation. This decrease, at around 5.2% each year, is most probably just a natural relaxation of pilgrim visitors to a ‘normal’ level rather than suggesting a lack of devotion. That being said, whilst the proportion of offerings to the total income was around 30% before the exile, in 1220 this proportion increased to 46% due to the vast number of pilgrims received. This was reinvested into the priory and Honorius III allowed one-quarter of these revenues from the Translation to be diverted towards rebuilding the cathedral chevet until its completion. As such, after the two decades of strife witnessed by the monks at Canterbury, the Translation and its offerings provided the necessary injection of income required to reach stability.

Conclusion

The danger, however, of a financial and administrative system of this scale within a monastic community which often saw its obedientiaries withdrawn from the priory was that it had the potential to detract the monks from the true essence of monastic life. As early as 1215-1216 in the treasurer accounts, a sum of £12. 2s. was found in the possession of a monk called Luke who had been tempted by proprietas and distracted from the Rule. As such, the two treasurers at Christ Church implemented a system of financial centralisation to control the flow of income and expenses, safeguard against autonomy, and inhibit possible greed. This was conducted in three ways.

Firstly, the treasurers assigned revenues to obedientiaries with a specific attached clause that stated the nature of the expenses that the aforementioned revenue was earmarked for. The accounts of 1221 illustrate, for example, the assignment of £74 16s. to the precentor for ‘ad opus refectorii’. Likewise in 1224, an expense of £168 10s. 5d. was assigned to John the Cellarer specifically for wood. As stated previously, the cellarer oversaw a vast amount of wealth which was why the treasurers implemented a second restriction whereby the tenure of an obedientiary was controlled on a rotation basis to safeguard the acquisition of wealth and influence. As aforementioned in the analysis of the cellarer, in 1221-1222 no less than three people occupied the office on a rotation cycle. To fully control the cellarer, however, a third restriction was implemented into the financial system whereby the creation of new officials limited the influence and financial responsibilities of any central obedientiaries. Within the expenses of 1216, £159 13s. 3d. was allocated to John the Kitchener (coquinarius). This role was briefly created in an attempt to deprive the cellarer of his most integral role – feeding the household. Nevertheless, by 1217 this was reabsorbed into the cellarer’s responsibility.

The culmination of these three limitations resulted in a productive and centralised administration with a degree of financial unity. The era of the 1220s was thus the beginning of an age marked by maximum financial control on behalf of the treasurers. Nevertheless, the expenses examined within this chapter shows that the monks lived comfortably and somewhat luxuriously with vast and costly expenses of food, wine, and wood, among other items, clearly demonstrating that the household was endlessly in debt. From various streams of revenues and continuous borrowing, the gap between income and expenditure was exceptionally slim. Equally, the peaks and troughs of the accounts altogether show that the priory had an unstable financial career which was heavily influenced by external factors.

By withdrawing from the individual obedientiaries, we can begin to better understand the topography of this elaborate web of offices under the supervision of the prior. Equally, we can see its growth. In the year 1213, reference was made in the financial accounts to two cellarers, two chamberlains, two sacrists, one almoner, and one garnerer. This, combined with an estimate of one precentor, succentor, infirmarian, refectorarian, five shrine-keepers, four estate wardens, a master of novices, two treasurers, and the prior would result in a complex hierarchy of at least 14 different offices with a minimum of 26 officials. This, however, does not include a later increase in the number of cellarers, nor does it include the lengthy list of sub-cellarers, sub-sacrists, and sub-chamberlains. This, in conjunction with David Knowles’ argument that by 1207 there were 77 monks at Christ Church, as well as J.B Sheppard’s analysis that “there were usually from 70 to 80 brethren on the books at one time”, it can be estimated these 26 obedientiaries oversaw around 50-60 monks. Be as that may, it also demonstrates that the administrative system of the priory was incredibly detailed, organised, and efficient.